Microfinance Sector | 04 Oct 2024

For Prelims: Microfinance, Marginalized groups, Women empowerment, Micro Finance Institutions (MFIs), Self Help Groups (SHGs), Poverty alleviation, Reserve Bank of India (RBI), Pradhan Mantri MUDRA Yojana, Indian Micro Finance Equity Fund (IMEF), E-Shakti initiative, Regional Rural Banks (RRBs), Cooperative societies

For Mains: Role of Microfinance Sector in Financial Inclusion

The microfinance sector is a crucial component of financial inclusion, offering small-value loans, savings, insurance, and other services to underserved populations. It plays a transformative role in poverty alleviation, women’s empowerment, and fostering entrepreneurship in developing economies.

What is Microfinance?

- About:

- Microfinance refers to providing financial services, including small-value loans, to households, small businesses, and entrepreneurs who lack access to formal banking services.

- It is an effective tool for financial inclusion, enabling marginalized and low-income groups, particularly women, to achieve social equity and empowerment.

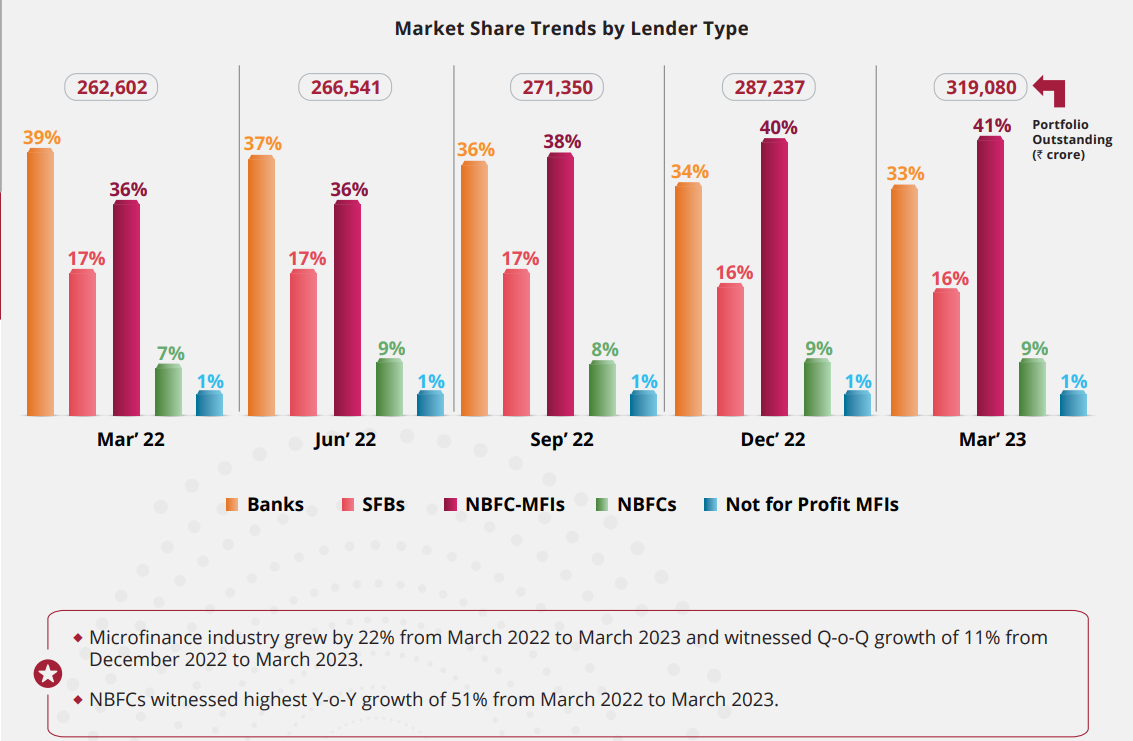

- In India, the microfinance sector has experienced significant growth, with 168 Micro Finance Institutions (MFIs) operating across 29 States, 4 Union Territories, and 563 districts.

- These MFIs serve over 3 crore clients with an outstanding loan portfolio of Rs. 46,842 crore.

- Evolution of the Microfinance Sector in India: The development of the microfinance sector in India occurred in four main phases:

- Initial Period (1974–1984):

- 1974: Shri Mahila Sewa Sahakari Bank was established to provide financial services to women in the unorganized sector.

- 1984: NABARD advocated Self Help Group (SHG) linkage as a tool for poverty alleviation.

- Change Period (2002–2006):

- 2002: Norms for unsecured lending to SHGs were aligned with other secured loans.

- 2004: The Reserve Bank of India (RBI) included microfinance within the priority sector, recognizing MFIs as a tool for financial inclusion.

- 2006: Allegations of high interest rates and unethical recovery practices led the government to shut down branches of some MFIs.

- Growth and Crisis (2007–2010):

- 2007: Private equity players entered the market, leading to rapid growth in the MFI loan book (INR 35 billion).

- 2009: The Microfinance Institutions Network (MFIN) was formed, allowing NBFC-MFIs to become members.

- 2010: The Andhra crisis unfolded, involving coercive debt collection practices that led to borrower suicides. The government issued an Ordinance, that significantly curbed MFI activities.

- Consolidation and Maturity (2012–2015):

- 2012: The Malegam Committee recommended changes, and RBI implemented new regulations.

- 2014: RBI issued a universal banking license to Bandhan Bank, the largest microlender. MFIN was recognized as a self-regulatory organization (SRO).

- 2015: The government launched MUDRA Bank to finance small businesses.

- Initial Period (1974–1984):

- Status of Microfinance in India:

- Microfinance contributes about 130 lakh jobs and 2% of our GVA, as per a National Council of Applied Economic Research (NCAER) study.

- It has the potential to reach all the 6.3 crore unincorporated and non-agricultural enterprises. The RBI recently defined microfinance as collateral-free loans given to households having annual incomes up to Rs. 3 lakh.

- Business Models in Microfinance:

- Self-Help Groups (SHGs):

- SHGs are informal groups of 10–20 members, mainly women, who pool their savings and become eligible for credit from formal banking institutions under the SHG-Bank Linkage Programme (SHG-BLP). NABARD plays a key role in developing and supporting SHGs.

- Microfinance Institutions (MFIs):

- MFIs provide micro-credit and other financial services like savings, insurance, and remittances. Loans are typically provided through Joint Lending Groups (JLGs), informal groups of 4–10 members engaged in similar economic activities who jointly repay loans.

- Self-Help Groups (SHGs):

- Categories of Microfinance Lenders:

- Non-Government Organizations (NGO-MFIs): Registered under the Society Registration Act 1860 or Indian Trust Act 1880, these NGOs extend micro-credit.

- Co-operative Societies: Registered under relevant laws, co-operative societies such as Primary Agricultural Credit Societies (PACS) offer microfinance services.

- Section 8 Companies (Formerly Section 25 of Companies Act 1956): These are non-profit entities that extend micro-credit under the Companies Act, 2013.

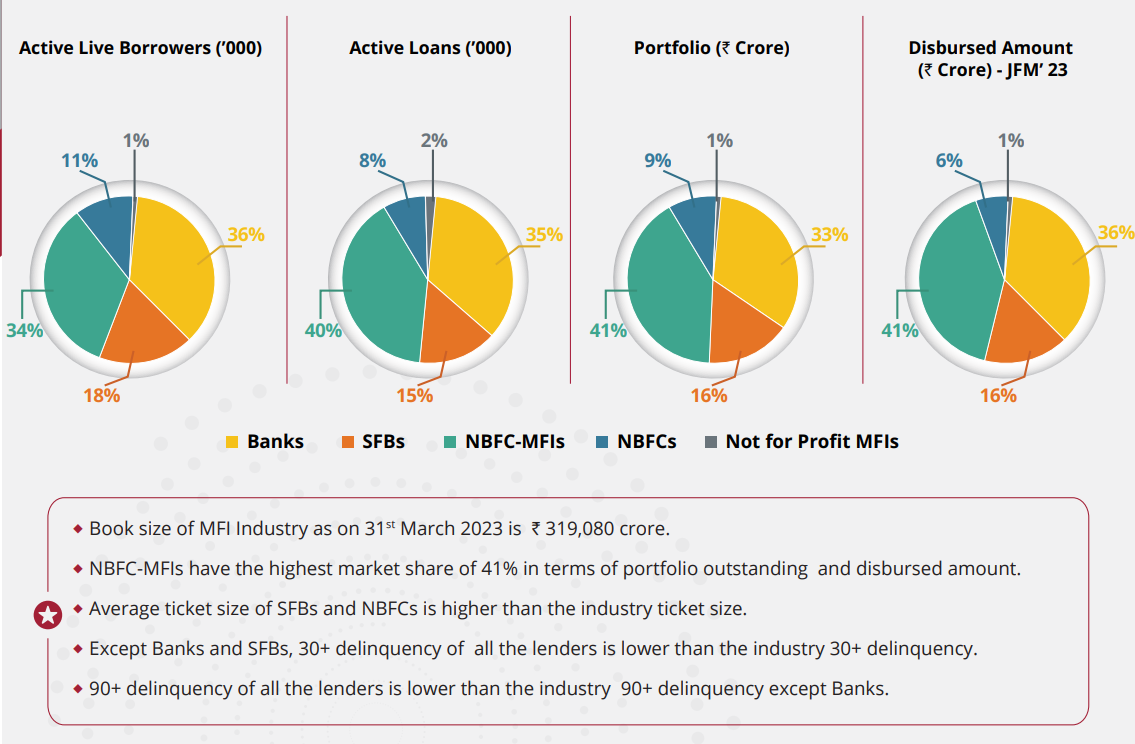

- Non-Banking Finance Companies (NBFC-MFIs): NBFC-MFIs raise funds from their own resources or bulk loans from banks to lend to JLGs. This category, introduced by the RBI in 2011, accounts for 80% of the microfinance market.

- Regulatory Framework:

- The Reserve Bank of India (RBI) regulates MFIs in India through the Non-Banking Financial Company-Micro Finance Institutions (NBFC-MFIs) framework, issued on 01.07.2014.

- The guidelines cover aspects like eligibility for registration, client protection, prevention of borrower over-indebtedness, privacy, and pricing of credit. MFIs generally comply with these regulations, contributing to stakeholder confidence in the sector.

What are the Government Measures for the Development of Microfinance Institutions (MFIs)?

- Indian Micro Finance Equity Fund (IMEF): To address liquidity challenges, the Government of India introduced the Indian Micro Finance Equity Fund (IMEF) in the Union Budget of 2011-12, with an initial allocation of Rs. 100 crore.

- Operated through the Small Industries Development Bank of India (SIDBI), this fund was aimed at strengthening the capitalization of smaller, socially oriented MFIs, particularly in underserved areas.

- Role of NABARD: NABARD's Micro Credit Innovations Department facilitates access to financial services for the unreached poor in rural areas through various microfinance innovations.

- Self Help Group – Bank Linkage Programme (SHG-BLP): SHG-BLP is a cost-effective model linking poor households to formal financial institutions.

- NABARD Financial Services Ltd. (NABFINS): NABARD established NABFINS as a model microfinance institution, focusing on governance, transparency, and reasonable interest rates.

- Micro Enterprise Development Programmes (MEDPs): Skill training for SHG members to enhance production activities.

- E-Shakti Initiative: The E-Shakti initiative, launched by NABARD, is a major technological advancement for the microfinance sector. The project focuses on mapping existing Self Help Groups (SHGs) and uploading both financial and non-financial information on a dedicated website.

- This digitization of SHGs improves transparency, enables better access to data, and facilitates more efficient financial inclusion efforts.

- Pradhan Mantri MUDRA Yojana (PMMY): Launched in 2015, the Pradhan Mantri MUDRA Yojana (PMMY) was introduced to enhance credit flow to small businesses, an essential component of financial inclusion.

How does Microfinance Contribute to Finacial Inclusion?

- Despite the significant achievements of the microfinance sector in recent years, there are numerous opportunities for further growth and development.

- Poverty Alleviation: Microfinance serves as a vital tool for alleviating poverty by providing access to financial services for low-income individuals and families.

- Studies have shown that microfinance can help lift people out of poverty, enabling them to diversify their income sources and improve their living conditions.

- Impact on Health, Social Capital, and Economy: Microfinance has a positive effect on various aspects of life, including health and education, which can subsequently influence economic development.

- For example, research indicates that providing mothers with access to credit can increase their children's school enrollment rates by approximately 1.9% for girls and 2.4% for boys, as observed by the Grameen Bank.

- Microfinance as a Development Tool: Microfinance can act as a buffer against unexpected crises, such as business risks or supply disruptions.

- Studies indicate that microfinance is relatively resilient to national and global economic fluctuations, offering a reliable support system during difficult times.

- Opportunity for Commercial Banks: With many Microfinance Institutions (MFIs) providing a limited range of microfinance products, there is an opportunity for commercial banks to develop innovative offerings in this sector.

- Research shows that microfinance products can have high recovery rates and profitability.

- Women Empowerment: Microfinance provides women with the opportunity to start and grow their businesses.

- Many MFIs, particularly in countries like Bangladesh, prioritize lending to women due to their higher repayment rates.

- Poverty Alleviation: Microfinance serves as a vital tool for alleviating poverty by providing access to financial services for low-income individuals and families.

What is the Concept of Financial Inclusion?

- About:

- Financial inclusion can be defined as "The process of ensuring access to financial services and timely, adequate credit, where needed, by vulnerable groups such as weaker sections and low-income groups, at an affordable cost."

- Challenges for Low-Income Households:

- Low-income households often lack access to bank accounts and face difficulties such as:

- Spending time and money on multiple visits to avail basic banking services

- Difficulty in opening savings accounts or accessing loans

- As a result, the unbanked population is largely disconnected from the banking system.

- Low-income households often lack access to bank accounts and face difficulties such as:

- Financial Exclusion:

- Certain trends, such as advanced customer segmentation technology, have restricted access to financial services for specific groups.

- This creates a divide, with high and upper-middle-income populations enjoying a wide range of personal finance options, while a significant portion lacks access to even basic banking services. This lack of access is termed "financial exclusion."

- Certain trends, such as advanced customer segmentation technology, have restricted access to financial services for specific groups.

- Conventional Models Failure in Financial Inclusion:

- Regional Rural Banks (RRBs): The establishment of Regional Rural Banks in 1975 aimed to extend formal credit systems to the rural population.

- The RRB Act, 1976 emphasized providing adequate and timely finance to the rural sector.

- Due to the predominance of the rural sector, RRBs have struggled with high levels of Non-Performing Assets (NPAs) and operational costs, resulting in heavy losses.

- Cooperatives: Rural credit cooperatives were established to pool the resources of people with small means and provide financial services to the poor in urban and rural areas.

- However, despite decades of cooperative efforts, private agencies continued to dominate the rural credit market, and cooperatives provided only 35% of the total borrowing needs of farmers.

- Regional Rural Banks (RRBs): The establishment of Regional Rural Banks in 1975 aimed to extend formal credit systems to the rural population.

What are the Challenges and Way Forward for India’s Microfinance Sector?

| Challenge | Way Forward |

| High outreach costs in remote areas. | Leverage technology, partner with local businesses, optimize field force |

| Over-indebtedness due to lack of proper assessment. | Strengthen risk assessment, provide financial education, diversify loan products. |

| Competitive disadvantage compared to mainstream banks. | Explore alternative funding sources, focus on value-added services, advocate for regulatory reforms. |

| Difficulty in acquiring reliable data for appraisals. | Develop standardized valuation frameworks, invest in data analytics, seek external validation. |

| Limited reach to the urban poor. | Tailor products and services, partner with urban local bodies, leverage digital channels. |

| Inadequate risk management practices and lack of collateral. | Enhance credit risk assessment, promote financial literacy, consider collateral requirements. |

| Difficulty in accessing clients in remote areas due to poor infrastructure. | Leverage mobile technology, partner with local agents, invest in infrastructure. |

| Limited operational flexibility and vulnerability to fluctuations in banking policies. | Explore alternative funding sources, build internal capacity, advocate for policy changes. |

| Lack of awareness regarding financial principles and services. | Conduct financial literacy campaigns, partner with schools and colleges, utilize digital platforms. |

| Limited product offerings, excluding low-wage workers from essential financial services. | Offer microinsurance, introduce savings products, explore digital payments. |

Conclusion

Micro Finance programme has played a significant role in the Indian economy. It has proved its viability as a business model as well as in its ability to reach out to a significant section of the population comprising the poor, the marginalised, and the unbanked. Acting in complementarity to the banking system, it has striven to provide sustainable microfinance services to the underprivileged, thereby providing more inclusive development and economic parity in the country.

UPSC Civil Services Examination, Previous Year Question (PYQ)

Prelims

Q. Microfinance is the provision of financial services to people of low-income groups. This includes both the consumers and the self-employed. The service/ services rendered under microfinance is/are (2011)

- Credit facilities

- Savings facilities

- Insurance facilities

- Fund Transfer facilities

Select the correct answer using the codes given below the lists:

(a) 1 only

(b) 1 and 4 only

(c) 2 and 3 only

(d) 1, 2, 3 and 4

Ans: (d)