Indian Economy

GST Council and Corporate Tax

- 21 Sep 2019

- 4 min read

The Goods & Services Tax (GST) Council held a meeting on 20th September 2019 to decide on tax moderation, keeping in mind the revenue position and the need to boost sagging economic growth.

- The GST Council had its 37th meeting in Goa in the backdrop of economic growth hitting a six-year low of 5% for the first quarter of the current fiscal (April - June 2019).

- There have been demands pouring in from various sectors — from biscuits to automobiles and Fast Moving Consumer Goods (FMCG) to hotels — to reduce tax rates in the wake of the economic slowdown.

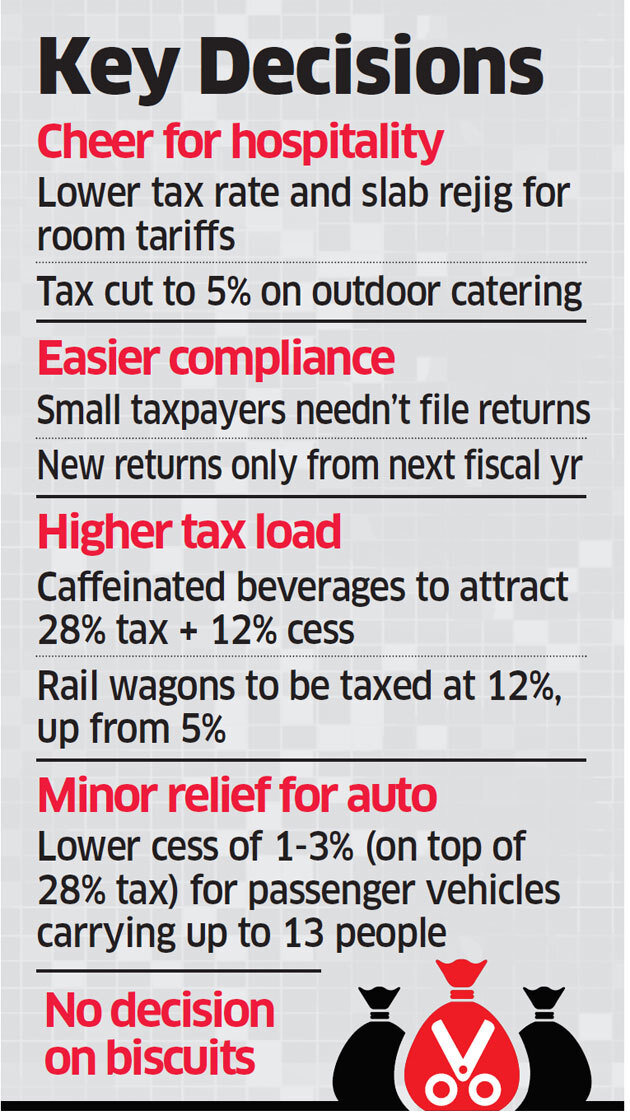

Decisions Taken

- To factor in the creation of Union Territories of Jammu and Kashmir as well as Ladakh, suitable amendments in the Central GST Act, the Union Territories’ GST Act, and the corresponding State GST Acts were approved.

- Slashed tax rates on a host of products and services, including jewellery stones, hotel stay and outdoor catering, besides easing the compliance burden for small and medium enterprises.

GST Council

- It is a constitutional body for making recommendations to the Union and State Government on issues related to Goods and Service Tax.

- The GST Council is chaired by the Union Finance Minister and other members are the Union State Minister of Revenue or Finance and Ministers in-charge of Finance or Taxation of all the States.

- It is considered as a federal body where both the centre and the states get due representation.

Corporate Tax Rate Slashed

- The central government slashed corporate tax rates for domestic firms from 30% to 22% and for new manufacturing companies from 25% to 15% to boost economic growth.

- Corporate tax is a tax imposed on the net income of the company.

- The new effective tax rate inclusive of surcharge and cess for domestic companies would be 25.17% and for new domestic manufacturing companies would be 17.01%.

- These rates would be applicable to those companies who forego the current exemptions and incentives.

- Also, the Minimum Alternate Tax (MAT) will not apply to such companies.

- The reduction in the corporate tax rate for domestic companies would be effective from 1st April 2019.

- The change for new domestic companies would apply for those which get incorporated on or after 1st October 2019 and start producing on or before 31st March 2023.

- The provisions affecting these changes have been inserted in the Income-tax Act through an ordinance.

- Impact:

- The move will cost the government Rs 1.45 lakh crore annually. This increases the chances of higher fiscal deficit and government may have to resort to spending cuts or embark on higher disinvestments.

- It is expected that it will give a great stimulus to ‘Make In India’, attract private investment from across the globe, improve the competitiveness of the private sector, create more jobs.

- The reduction in corporate tax, effectively, brings India’s ‘headline’ corporate tax rate broadly at par with an average of 23% rate in Asian countries.