-

28 Feb 2025

GS Paper 3

Economy

Day 77: The Goods and Services Tax (GST) has transformed India’s indirect tax system into a single framework, advancing the "One Nation, One Tax" vision. How has GST streamlined tax administration and compliance, and what further measures are required to improve its effectiveness? (250 words)

Approach

- Introduce Goods and Services Tax (GST) and the Concept of "One Nation, One Tax”.

- Explain how GST streamlines tax administration and compliance.

- Highlight challenges in GST implementation.

- Suggest measures to enhance GST effectiveness.

- Conclude suitably.

Introduction

The introduction of the Goods and Services Tax (GST) in India in 2017 marked a significant step toward realizing the vision of "One Nation, One Tax," aiming to create a unified tax structure. GST sought to replace the fragmented indirect tax system, which consisted of multiple taxes like VAT, excise duty, and service tax, levied by the central and state governments. By streamlining tax administration and compliance, GST has paved the way for greater transparency, efficiency, and economic integration.

Body

Streamlining Tax Administration and Compliance under GST:

- GST Base Expansion: The number of GST taxpayers increased from 6 million in FY 2017-18 to over 12 million in FY 2020-21. (GSTN Annual Report 2020-21)

- Revenue Growth: GST revenue exceeded ₹1 lakh crore per month for several months in FY 2021-22, reflecting the system's effectiveness in tax collection.

- GST Network (GSTN):

- A digital platform that automates processes such as tax filing, returns, and payments, reducing human intervention.

- Example: Over 1.2 billion GST returns filed in FY 2020-21, showing the scale of digital compliance.

- Input Tax Credit (ITC):

- The ITC mechanism ensures businesses only pay tax on value-added portions, eliminating the cascading tax effect.

- Example: NIPFP study shows that cascading taxes could reduce by over 40%, lowering production costs and stabilizing prices.

- GST Returns Filing:

- The GSTR 1, GSTR 2, and GSTR 3B system helps track sales and purchase details across the supply chain, improving transparency.

- Challenge: Initially, the frequent filing of returns was cumbersome but has been simplified over time.

- Anti-Profiteering Authority:

- Ensures businesses pass on tax benefits to consumers.

- Example: In 2018, the authority took action against businesses that did not pass on GST benefits to consumers.

- SMEs Benefit: Small and Medium Enterprises (SMEs) benefited from the Composition Scheme, which simplified tax filing and reduced compliance burdens.

- Example: GST registration for businesses with annual turnover up to ₹1.5 crore can opt for a simplified tax structure.

Challenges Faced in GST Implementation:

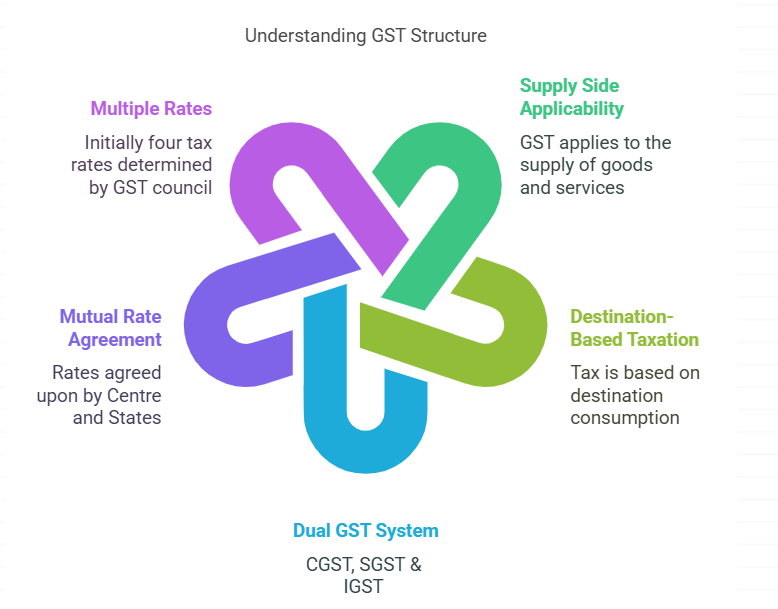

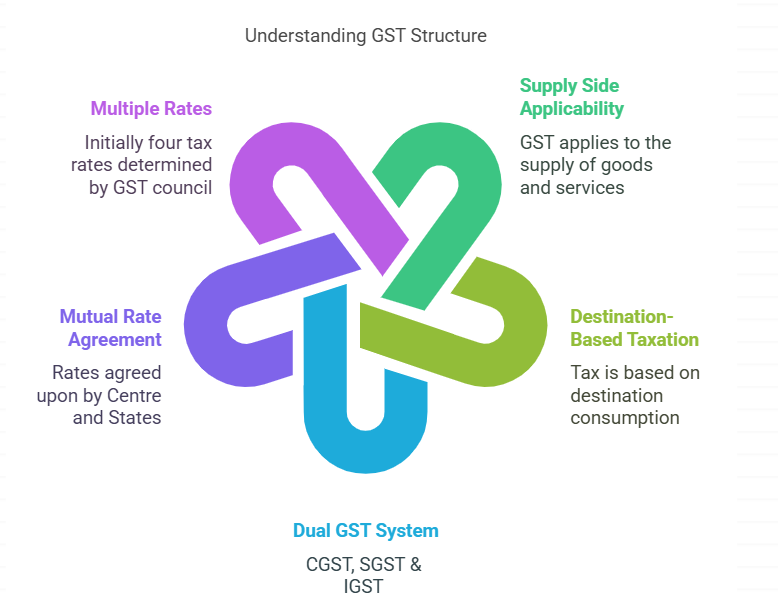

- Complex Rate Structure:

- GST’s multi-slab system (5%, 12%, 18%, 28%) has led to confusion, particularly in sectors like real estate and construction.

- ITC Reconciliation:

- Issues arose when purchase invoices didn’t match sales tax credits, leading to delays and discrepancies.

- Compliance Burden on Small Businesses:

- Small businesses, especially in the informal sector, faced difficulties in meeting compliance requirements due to digitalization.

- Slow Inclusion of Unorganized Sector:

- Despite efforts, sectors like agriculture and construction, where documentation is minimal, lagged in GST adoption.

- Impact on Cooperative Federalism – Disputes between the Centre and states over GST compensation cess payments have strained federal relations.

Measures for Improving GST Effectiveness:

- Simplify the Rate Structure:

- Rationalize the multi-slab system to fewer tax brackets or a single tax rate, reducing confusion and enhancing compliance.

- Streamline IT Systems:

- Integrate IT systems to allow automatic reconciliation of Input Tax Credit (ITC), reducing discrepancies and delays in refunds.

- Quarterly Filing for Small Businesses:

- Introduce quarterly return filing for all businesses, especially SMEs, to reduce the administrative burden.

- Improving Centre-State Coordination:

- Strengthening cooperative federalism through regular consultations in the GST Council can address state concerns effectively.

- Increase Awareness and Training:

- Focus on targeted programs for small businesses, the informal sector, and industries like agriculture to ensure smooth GST adoption and compliance.

Conclusion

GST has significantly advanced the vision of "One Nation, One Tax" by simplifying tax administration and reducing the cascading tax effect. Continued reforms to streamline the rate structure, enhance digital infrastructure, and support small businesses can further improve GST’s effectiveness and its ability to boost India’s economic growth and tax compliance.