Seven Years of Pradhan Mantri Jan Dhan Yojana

Why in News

Recently, the government has asked the banks to improve access of account holders in the Pradhan Mantri Jan Dhan Yojana (PMJDY) scheme to micro-credit and micro investment products, like flexi-recurring schemes.

- PMJDY - National Mission for Financial Inclusion has completed seven years of successful implementation.

Key Points

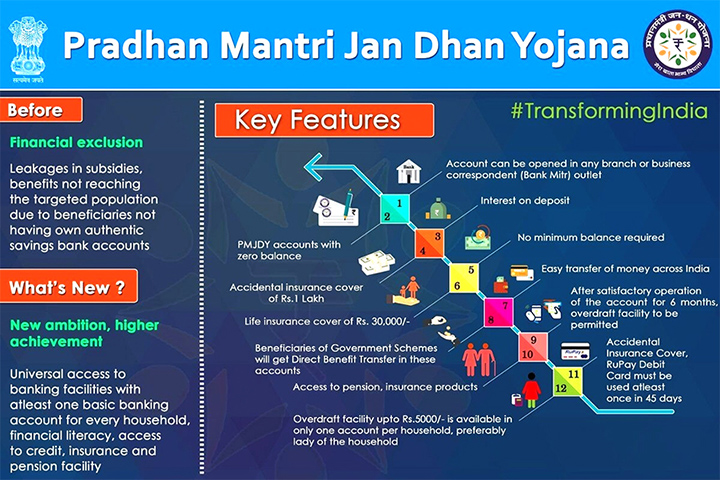

- Objective of PMJDY:

- Ensuring access to various financial services to the excluded sections i.e. weaker sections & low income groups at an affordable cost and using the technology for the same.

- Six Pillars of the Scheme:

- Universal Access to Banking Services – Branch and Banking Correspondents.

- Accounts opened are online accounts in the core banking system of banks.

- Focus has shifted from ‘Every Household’ to Every Unbanked Adult’.

- Basic Savings Bank Accounts with OverDraft (OD) Facility of Rs. 10,000/- to every household.

- Financial Literacy Program– Promoting savings, use of ATMs, using basic mobile phones for banking, etc.

- Creation of Credit Guarantee Fund – To provide banks some guarantee against defaults.

- Insurance – Free accidental insurance cover on RuPay cards increased from Rs. 1 lakh to Rs. 2 lakh for PMJDY accounts opened after August 2018.

- Pension Scheme for the Unorganized sector.

- Universal Access to Banking Services – Branch and Banking Correspondents.

- Achievements:

- Accounts:

- The number of accounts rose to 43.04 crore in August 2021 from 17.9 crore in August 2015.

- Of this, 55.47% Jan Dhan account holders are women and 66.69% holders are in rural and semi-urban areas.

- Deposits:

- The deposits have shot up to Rs. 1.46 lakh crore from Rs. 22,901 crore during 2015-2021.

- Operative Accounts:

- As per extant Reserve Bank of India guidelines, a PMJDY account is treated as inoperative if there are no customer induced transactions in the account for over a period of two years.

- In August 2021, out of total 43.04 crore PMJDY accounts, 36.86 crore (85.6%) were operative.

- Continuous increase in percentage of operative accounts is an indication that more and more of these accounts are being used by customers on a regular basis.

- As per extant Reserve Bank of India guidelines, a PMJDY account is treated as inoperative if there are no customer induced transactions in the account for over a period of two years.

- RuPay Usage:

- Number of RuPay cards & their usage has also increased over time.

- Jan Dhan Darshak App:

- This app is being used for identifying villages which are not served by banking touchpoints within 5 km. The efforts have resulted in a significant decrease in the number of such villages.

- Pradhan Mantri Garib Kalyan Package (PMGKP) for PMJDY Women:

- Under PMGKP, a total of Rs. 30,945 crore have been credited in accounts of women PMJDY account holders during Covid lockdown.

- Smooth DBT Transactions:

- About 5 crore PMJDY account holders receive Direct Benefit Transfer (DBT) from the Government under various schemes.

- Accounts:

- Impact:

- Increased Financial Inclusion:

- PMJDY has been the foundation stone for people-centric economic initiatives. Whether it is DBT, Covid-19 financial assistance, PM-KISAN, increased wages under MGNREGA, life and health insurance cover, the first step of all these initiatives is to provide every adult with a bank account, which PMJDY has nearly completed.

- Formalisation of Financial System:

- It provides an avenue to the poor for bringing their savings into the formal financial system, an avenue to remit money to their families in villages besides taking them out of the clutches of the usurious money lenders.

- Prevention of Leakage:

- DBTs via PM Jan Dhan accounts have ensured every rupee reaches its intended beneficiary and prevents systemic leakage.

- Increased Financial Inclusion:

- Challenges:

- Connectivity:

- Lack of physical and digital connectivity is posing a major hurdle in achieving financial inclusion for rural India.

- Technological Issue:

- The technological issues affecting banks from poor connectivity, networking and bandwidth problems to managing costs of maintaining infrastructure especially in rural areas.

- Procedure not Clear:

- Most of the people are aware but still so many are not turned around as they are not understanding the proper procedure of opening an account and required documents at a time.

- Connectivity:

Way Forward

- There must be an endeavour to ensure coverage of PMJDY account holders under micro insurance schemes.

- Eligible PMJDY account holders will be sought to be covered under Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY).

- Promotion of digital payments including RuPay debit card usage amongst PMJDY account holders through creation of acceptance infrastructure across India.