Insurance Sector in India

This article is based on “Keeping it Saral” which was published in The Hindu Businessline on 22/10/2020. It talks about the journey of the insurance sector in India and its associated issues.

Insurance is the main element in the operation of national economies throughout the world today. It protects health and assets of the people and stimulates business activities to operate in a cost-effective manner.

Citing this, the Insurance Regulatory and Development Authority (IRDA) has released guidelines for the insurance sector i.e. Saral Jeevan Bima (SJB). Saral Jeewan Bima provides for broad contours of a standard individual term life insurance product which must be adhered by insurance companies.

While India’s insurance sector has been growing dynamically in recent years, its share in the global insurance market remains abysmally low.

There are many underlying issues which affect the insurance sector in India such as low penetration and density rates, inadequate investment in insurance products, and the dominant position and deteriorating financial health of public-sector players.

Therefore, the goal of making insurance accessible to all will remain difficult to achieve, until the above mentioned issues are addressed.

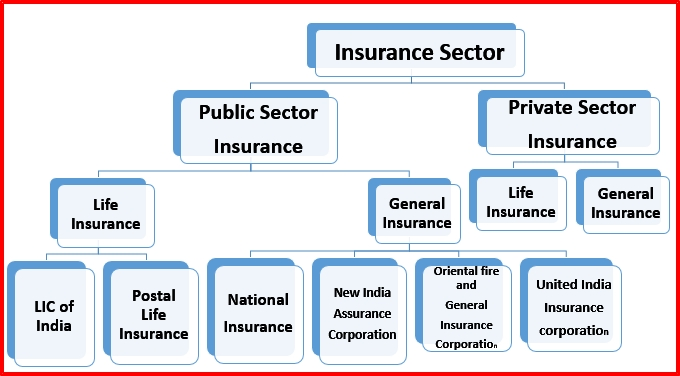

Background of Insurance Sector

The insurance sector has witnessed many changes over the years including:

- Nationalisation of life (LIC Act 1956) and non-life sectors (GIC Act 1972).

- Constitution of the Insurance Regulatory and Development Authority of India (IRDAI) in 1999.

- Opening up of the sector to both private and foreign players in 2000.

- Increase in the foreign investment cap to 26% from 49% in 2015.

- The recent notification of 100% foreign direct investment (FDI) for insurance intermediaries (announced in the Union Budget of 2019-20) has further liberalised the sector.

Saral Jeevan Bima

With SJB, IRDA envisages to increase penetration of insurance in India. Under this scheme:

- Standardisation: IRDA has come up with guidelines for a “standard" product—Saral Jeevan Bima—specifying the terms and conditions, benefits, and features that life insurance companies must include. Thereby, making it simpler for individuals to buy a term insurance policy.

- SJB will make it easier for the customers to make an informed choice, enhance the trust between the insurers and the insured, and reduce mis-selling as well as potential disputes at the time of claiming settlement.

- Inclusive: The product guidelines mention that insurers should offer the product without restrictions on gender, place of residence, travel, occupation, or educational qualifications.

- Securing Interests of Insurers: Insurers will not be liable for a payout if the policyholder dies within 45 days of taking the policy except in case of accident.

Challenges in India’s Insurance sector

- Prevalence of Insurance Gap: The insurance penetration (ratio of total premium to GDP (gross domestic product)) and density (ratio of total premium to population) stood at 3.69% and US$ 73, respectively for FY18 (fiscal year 2017-18), which is low in comparison with global levels.

- These low penetration and density rates reveal the uninsured nature of large sections of population in India, and the presence of an insurance gap.

- Public Sector Dominated: The insurance sector has transitioned from being an exclusive State monopoly to a competitive market, but public-sector insurers hold a greater share of the insurance market even though they are fewer in number.

- Nascent Non-life Insurance: Life insurance dominates the sector with a huge share of 74.7%, with non-life insurance accounting for the remaining 25.3%.

- In the non-life insurance sector, motor, health, and crop insurance segments are driving growth. India’s non-life insurance penetration is below 1%.

- In addition, insurance products catering to speciality risks such as catastrophes and cyber security are at a nascent stage of development in the country.

- Rural-Urban Divide: Low insurance penetration and density rates prevail in India. However, Rural participation of insurers remains deficient, and life insurers, especially private ones, gravitate towards the urban population.

- Capital Starved Insurers: Insurers in India lack sufficient capital, and their financial health, particularly that of the public-sector insurers, is in a precarious state.

- Further, investment in the insurance sector got dwindled due to the crisis in banks and NBFCs (non-banking financial companies) sector.

Way Forward

- Rural Centric Approach: Insurance companies in India will have to show long-term commitment to the rural sector as well, and will have to design products which are suitable for rural people.

- In this context, government insurance schemes such as Pradhan Mantri Jan Arogya Yojana, Pradhan Mantri Fasal Bima Yojana, Pradhan Mantri Suraksha Bima Yojana, and Pradhan Mantri Jeevan Jyoti Bima Yojana are notable steps in right direction.

- Need For Awareness Program: There is a need for complementary thrust to spread awareness and improve financial literacy, particularly the concept of insurance, and its importance.

- Technological Intervention: Another area that necessitates regulatory scrutiny is that of application of technology in insurance. An example is the emergence of ‘InsurTech’, designed to make the claim process simpler and more comprehensible.

- Enhanced Role of Regulator: The regulator needs to exercise vigilance on three other aspects.

- It must ensure that insurance is not denied to lower-income people who make up the bulk of the population and have the most need for protection.

- It should insist that insurers facilitate a simple online process for direct buying of insurance products, bypassing intermediaries.

- It should ensure that players do not overcharge or add hidden costs.

Conclusion

Demographic factors, coupled with increasing awareness and financial literacy, are likely to catalyse the growth of the sector. An enhanced regulatory regime that focuses on increasing insurance coverage is the need of the hour.

|

Drishti Mains Question Discuss the significance of the insurance sector in Indian economy and its underlying issues. |