Indian Economy

Privatisation of Public Sector Banks

- 12 Jun 2020

- 7 min read

This article is based on “Privatisation is not a panacea for PSBs” which was published in The Hindu business line on 11/06/2020. It talks about the pros and cons of privatisation of Public sector banks.

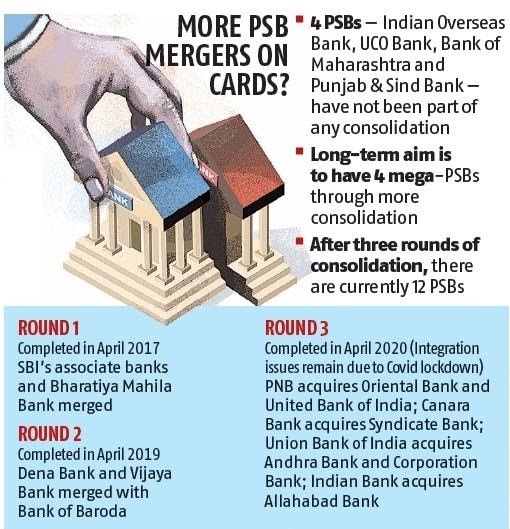

Recently, the union government has stated that it is considering to designate the banking sector as a strategic under the new privatisation policy- announced as a part of the ‘Atmanirbhar Bharat’ package.

The new privatisation policy envisages that in each strategic sector, no more than four state-owned companies will exist. Currently, after the latest round of consolidation, there are 12 public sector banks (PSBs).

This means having four mega PSBs will either come through further mergers of PSBs or privatisation. Privatisation is often considered a solution for poor management in public sector banks.

However, former governor of RBI Raghuram Rajan held that privatisation is not a panacea for the ills of the banking sector unless accompanied by reforms in banking regulation.

Rationale of Privatization of PSBs

- Bulk of NPAs: The banking system is overburdened with the non-performing assets (NPAs) and the majority of which lies in the public sector banks.

- Issue of Dual Control: PSBs are dually controlled by RBI (under the RBI Act, 1934) and Finance Ministry (under the Banking Regulation Act, 1949)

- Thus, RBI does not have all the powers over PSBs that it has over private sector banks, such as the power to revoke a banking licence, merge a bank, shut down a bank, or penalize the board of directors.

- Lack of Autonomy: Public sector bank boards are still not adequately professionalized, as the government still decides board appointments (as the Bank Bureau board is not fully functional). This creates an issue of politicization and interference in the normal functioning of Banks.

- Difference of Incentives: Private and public sector banks are driven by different incentives.

- For example, Private banks are profit-driven whereas the business of PSBs is disrupted by governments schemes like farm loan waivers etc.

- Also, in the private sector, the shareholders’ effective control over banks may explain the absence of large-scale frauds like in public sector banks such as the Punjab National Bank episode.

Issues Related to Privatization of Banks

- Issue of Governance: The key issue of Indian banking is a lack of adequate governance which stretches across public and private ownership.

- In the case of PSBs, there is political interference while private banks are prone to malpractices in the wake of serving the interest of its promoters.

- The testimony that the problems of Indian banking transcend issues of ownership lies in the plight of YES Bank.

- Policy Issue: Restructuring schemes such as corporate debt restructuring, strategic debt restructuring and schemes for sustainable structuring of stressed assets, initiated by RBI, are the major reasons for delaying the recognition of bad loans, which are irrespective of ownership (public as well as private) of the banks.

- Failure of Regulation: As RBI may not have similar control over PSBs as with respect to private banks, this does not explain why the RBI cannot hold the PSBs accountable for issues such as capital adequacy, fraud control or appropriate reporting of financial statements.

- RBI is well legislatively equipped to regulate banks under the RBI Act.

Note: Under the RBI Act

- The RBI can control the lending policy of PSBs, including determining maximum exposure, and the purpose of lending.

- The RBI approves the auditor for PSBs and has the power to issue special audits on PSU banks.

- RBI can inspect PSBs just like private sector banks, and give directions, including directions on management.

- It can appoint RBI officers to attend board meetings of PSBs and speak in them, collect all communications of a PSB’s board, and require them to make changes in management (except board).

- RBI can ask PSBs to maintain records as per rules made by RBI, impose penalties on PSU banks through the courts or directly under RBI systems.

- PSBs as an Instrument for Social Justice: PSBs also act as an instrument for social justice as they execute many welfare policies like financial inclusion, farm loan waiver etc.

Way Forward

- Improving Governance: In order to improve the governance and management of PSBs, there is a need to implement the recommendations of the PJ Nayak committee.

- De-Risking Banks: There is a need to follow prudential norms for lending and NPAs can be tackled through the establishment of the bad bank and speedy resolution of NPAs through Insolvency Bankruptcy Code.

- Corporatisation of PSBs: Rather than blind privatisation, PSBs can be made into a corporation like Life Insurance Corporation (LIC). While maintaining government ownership, this will give more autonomy to PSBs.

|

Drishti mains Question “Privatisation of Public sector banks may be necessary but not a sufficient reform to address the issues pertaining to ailing Indian banking sector”. Critically Examine. |

This editorial is based on “Assam OIL blowout, fire: The polluter must pay” which was published in The Hindustan Times on June 11th, 2020. Now watch this on our Youtube channel.