National Strategy for Financial Education | 21 Aug 2020

Why in News

The Reserve Bank of India (RBI) has released the National Strategy for Financial Education (NSFE): 2020-2025 document for creating a financially aware and empowered India.

- It is the second NSFE , the first one being released in 2013.

Key Points

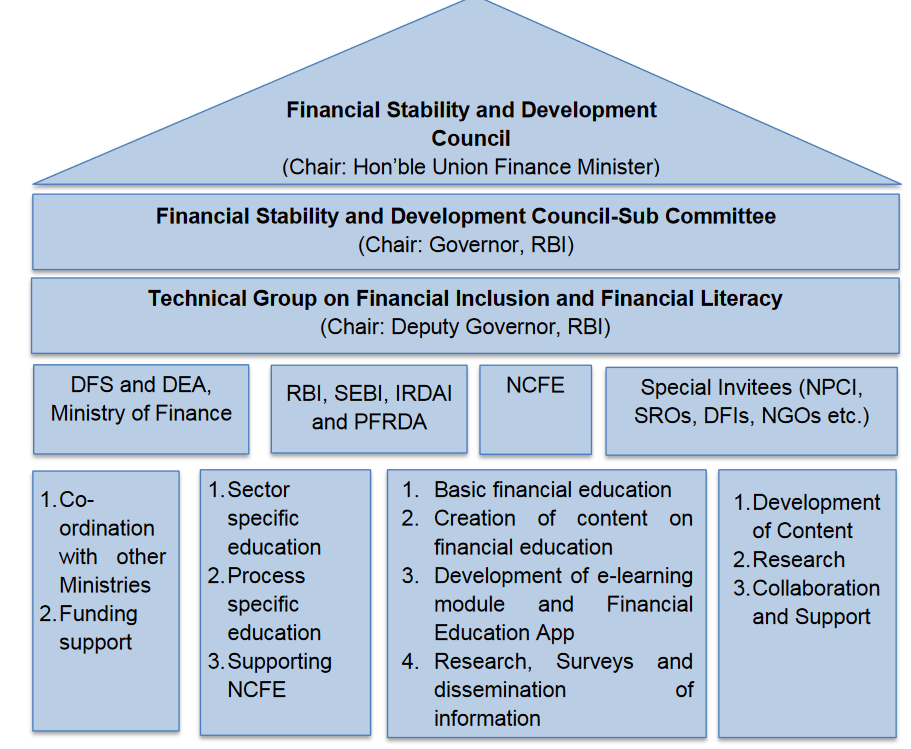

- This NSFE for the period 2020-2025 has been prepared by the National Centre for Financial Education (NCFE) in consultation with all the Financial Sector Regulators viz. RBI, Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI), Pension Fund Regulatory and Development Authority (PFRDA), etc. under the aegis of the Technical Group on Financial Inclusion and Financial Literacy (TGFIFL).

- NCFE is a Section 8 (Not for Profit) Company under the Companies Act, 2013 promoted by RBI, SEBI, IRDAI and PFRDA.

- It emphasizes a multi-stakeholder-led approach for empowering various sections of the population to develop adequate knowledge, skills, attitudes and behaviour which are needed to manage their money better and to plan for the future i.e. ensuring their financial well-being.

- It has recommended a ‘5 C’ approach for dissemination of financial education in the country:

- Content: Financial Literacy content for various sections of population.

- Capacity: Develop the capacity and ‘Code of Conduct’ for financial education providers.

- Community: Evolve community led approaches for disseminating financial literacy in a sustainable manner.

- Communication : Use technology, media and innovative ways of communication for dissemination of financial education messages.

- Collaboration : Streamline efforts of other stakeholders for financial literacy.

- Strategic Objectives:

- Inculcate financial literacy concepts among the various sections of the population through financial education to make it an important life skill.

- Encourage active savings behaviour.

- Encourage participation in financial markets to meet financial goals and objectives.

- Develop credit discipline and encourage availing credit from formal financial institutions as per requirement.

- Improve usage of digital financial services in a safe and secure manner.

- Manage risk at various life stages through relevant and suitable insurance cover.

- Plan for old age and retirement through coverage of suitable pension products.

- Knowledge about rights, duties and avenues for grievance redressal.

- Improve research and evaluation methods to assess progress in financial education.

- The Strategy also suggests adoption of a robust ‘Monitoring and Evaluation Framework to assess the progress made.

- TGFIFL would be responsible for periodic monitoring and implementation of NSFE under the oversight of Financial Stability and Development Council (FSDC).

- TGFIL was set up in November 2011 by the FSDC.

- Recently, RBI also released the National Strategy for Financial Inclusion (NSFI) for the period 2019-2024.

- It is an ambitious strategy which aims to strengthen the ecosystem for various modes of digital financial services in all Tier-II to Tier VI centres to create the necessary infrastructure to move towards a less-cash society by March 2022.

Financial literacy

- According to the Organization for Economic Co-operation & Development (OECD), it is defined as a combination of financial awareness, knowledge, skills, attitude, and behaviour necessary to make sound financial decisions and ultimately achieve individual financial well-being.

Financial Education

- It is defined as the process by which financial consumers/investors improve their understanding of financial products, concepts and risks and through information, instruction and/or objective advice, develop the skills and confidence to become more aware of financial risks and opportunities, to make informed choices, to know where to go for help and to take other effective actions to improve their financial well-being.

Way Forward

- India has made tremendous progress in bringing its citizens into the formal financial system over the last many years. Many important financial inclusion initiatives have been taken by the government such as Pradhan Mantri Jan-Dhan Yojana, social security schemes viz. Pradhan Mantri Jeevan Jyoti Bima Yojana, Pradhan Mantri Suraksha Bima Yojana, Atal Pension Yojana, Pradhan Mantri Kisan Maan Dhan Yojana, Pradhan Mantri Shram Yogi Mann Dhan Yojana (PM-SYM) and Pradhan Mantri Mudra Yojana.

- The latest available World Bank’s Findex 2017 Report had brought out that the proportion of adults with a formal account in the country has risen from 35% in 2011, to 80% in 2017.

- However,the country still needs to tread a long path to achieve a respectable financial literacy rate which is crucial for inclusive growth. For this besides the already existing delivery channels for disseminating financial education messages, newer modes such as social media platforms, should be effectively deployed.