GST on Health and Life Insurance in India | 09 Aug 2024

For Prelims: National Health Policy (NHP), Ayushman Bharat PMJAY, Insurance Regulatory and Development Authority of India, Health Insurance, World Health Organisation, Goods and Services Tax (GST)

For Mains: GST on Health and Life Insurance in India, Issues and Challenges with High Taxes on Insurances, India Health Infrastructure- Challenges and Way Forward, Challenges associated with ensuring the effective use of increased Healthcare funds in India.

Why in News?

Recently, the debate surrounding the Goods and Services Tax (GST) on health and life insurance has gained momentum, particularly following protests led by opposition leaders demanding the withdrawal of the 18% GST on insurance premiums.

- The rising cost of premiums, exacerbated by this tax, has made insurance increasingly unaffordable for many citizens, prompting discussions in Parliament and among industry stakeholders.

What is the Current State of Health Expenditure in India?

- Higher Medical Inflation:

- India's healthcare expenditure has been under scrutiny, with medical inflation estimated at around 14% towards the end of 2023.

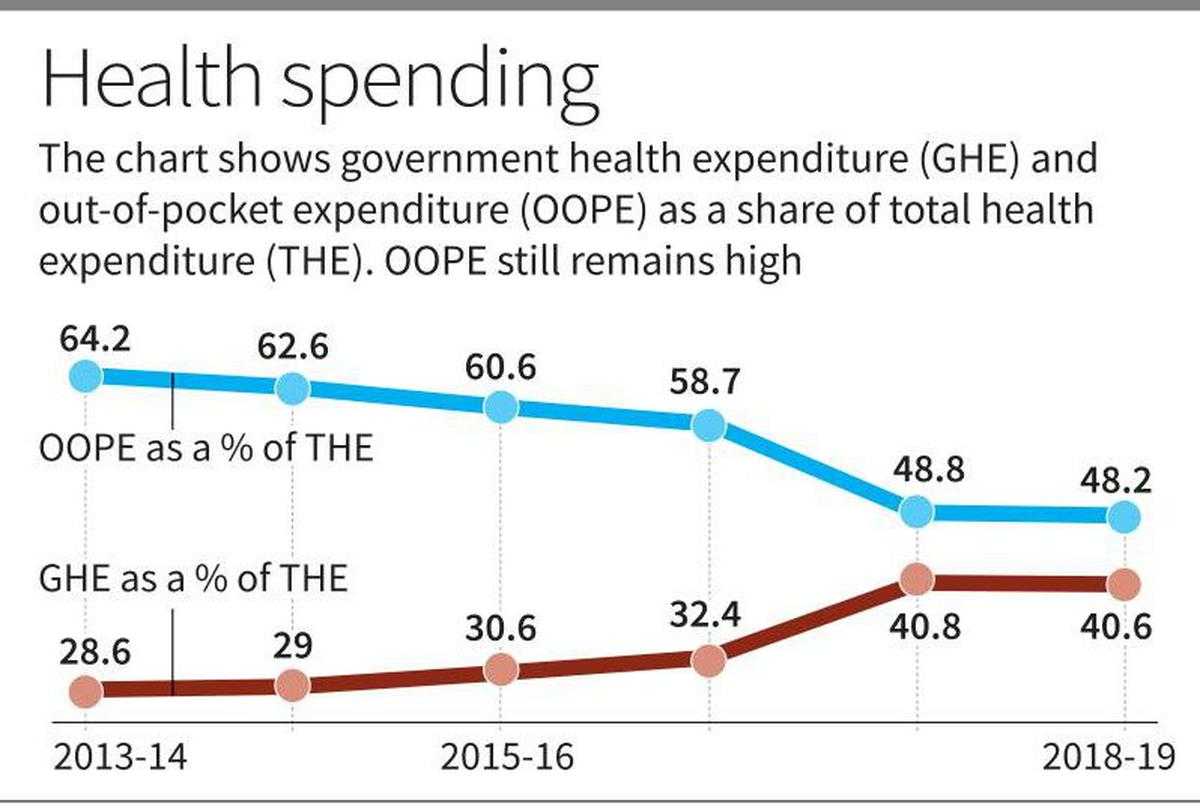

- Higher Out-of-Pocket Expenditure (OOPE):

- Out-of-Pocket Expenditure (OOPE) is still around 39.4% of Total Health Expenditure (THE) in 2021-22 as per National Health Accounts (NHA) data.

- Although this has dropped significantly from 62.6% in 2014-15 to 39.4% in 2021-22.

- In states such as Uttar Pradesh, the OOPE were as high as 71.3%.

- Marginal Increase in Government Health Expenditure (GHE):

- The share of Government Health Expenditure (GHE) in Total Health Expenditure (THE) has risen from 28.6% in 2013-14 to just 40.6% in FY19.

- GHE as a percentage of GDP increased 63% between 2014-15 to 2021-22, rising from 1.13% of GDP in 2014-15 to 1.84% by 2021-22.

- Share of Health Expenditure in GDP: In the year 2019-20, India's Total Health Expenditure (THE) was estimated at Rs. 6,55,822 crores, which represents 3.27% of the GDP and amounts to Rs. 4,863 per capita.

- In comparison, countries like the US spend about 18% of their GDP on healthcare, while countries such as Germany and France spend around 11-12%.

Why is there Need to Reduce GST on Health and Life Insurance Premiums?

- Insurance a Basic Necessity: Insurance is a basic necessity as it provides financial protection against unexpected events, safeguarding family's financial interests and thus it should not be subjected to high taxes.

- Affordability: The 18% GST on insurance premiums significantly increases the cost for policyholders. With health insurance premiums having risen by up to 50% in some cases, many individuals are finding it increasingly difficult to maintain their policies.

- Global Comparison: The GST on insurance in India is among the highest in the world. Countries like Singapore and Hong Kong do not impose such taxes on insurance, making their insurance products more attractive and affordable.

- Impact on Insurance Penetration: The high GST rate contributes to low insurance penetration in India, which was only 4% in 2022-23, lower than the global average of around 7%.

- Lowering the GST could encourage more people to purchase insurance, aligning with the goal of "Insurance for All by 2047."

- Economic Growth: Taxing insurance premiums can restrict the growth of the insurance sector, which is vital for economic stability and individual financial security.

What can be the Downsides of Removing GST on Life and Health Insurance?

- Revenue Loss for Governments: GST from life and health insurance (@ 18%) generates significant revenue for federal and state governments. Removing it could lead to budget deficits, affecting funding for public health initiatives and services.

- Increased Burden on Other Taxpayers: To compensate for the lost revenue, governments may need to increase other taxes, placing a heavier burden on taxpayers.

- Potential for Increased Prices: While removing GST may seem to lower costs for consumers, healthcare providers might increase prices to maintain revenue levels, negating the intended benefits.

India's Insurance and Pension Sector: A Growth Opportunity

- Global Comparison and Opportunity for Growth:

- India's insurance and pension sectors lag behind global counterparts. While these sectors contribute 19% and 5% to India's GDP, respectively, developed economies like the US (52% and 122%) and the UK (112% and 80%) showcase significantly higher penetration.

- This gap presents a substantial opportunity for growth in India's insurance and pension markets.

- India's insurance and pension sectors lag behind global counterparts. While these sectors contribute 19% and 5% to India's GDP, respectively, developed economies like the US (52% and 122%) and the UK (112% and 80%) showcase significantly higher penetration.

- Industry Performance:

- The General Insurance sector collected Rs 1,09,000 crore in health premiums alone during FY 2023-24.

- The Life Insurance industry mobilised Rs 3,77,960 crore in premiums in FY 2024, with LIC contributing the majority at Rs 2,22,522 crore.

Way Forward

- GST Review: The government should consider reviewing the GST on health and life insurance premiums to make them more affordable and encourage higher penetration rates.

- A parliamentary committee, chaired by the former MoS Finance, has proposed reducing GST on health and term insurance to lower premiums and encourage policy uptake.

- Capital Support to Insurance Sector: Parliamentary committee suggests that the Reserve Bank of India issue 'on-tap' bonds to meet the insurance sector's capital requirements, estimated at Rs 40-50,000 crore.

- "On-tap bonds" refer to bonds that are available for purchase at any time, rather than being issued in a specific offering or auction.

- More Public Investments in Healthcare: Increased public investment in healthcare in developing countries shows that higher spending leads to greater utilisation of services. As healthcare becomes more affordable, latent demand is realised, enabling more people to access care.

- Investments in More Medical Colleges: To bring down costs beyond a few islands of excellence such as the AIIMS, investments in other medical colleges shall be encouraged to possibly bring down costs and ramp up quality of health services.

- Policy Reforms: Policy reforms to reduce medical inflation and control healthcare costs can enhance health insurance affordability. Additionally, offering incentives to insurers can promote competition and innovation, further lowering costs.

|

Drishti Mains Question: What are the challenges related to the healthcare sector in India? What steps can be taken to make health services more affordable? |

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Mains:

Q. “Besides being a moral imperative of a Welfare State, primary health structure is a necessary precondition for sustainable development.” Analyse. (2021)