Indian Economy

External Benchmarks Lending Rate

- 20 Jul 2021

- 7 min read

Why in News

According to a recent RBI report on ‘Monetary transmission in India’, the share of outstanding loans linked to External Benchmarks Lending Rate (EBLR - like repo rate), increased from as low as 2.4% during September 2019 to 28.5% during March 2021.

- This increase in EBLR linked lending will contribute to significant improvement in monetary policy transmission.

- However, still 71.5% of outstanding loans are Internal Benchmark Lending Rate (IBLR- like base rate and MCLR) linked loans, which continues to impede the monetary policy transmission.

Note

- Transmission of Monetary Policy: The transmission of monetary policy describes how changes made by the Reserve Bank of India (RBI) to the policy rate flow through to economic activity (like lending) and inflation.

- Repo Rate: It is also known as the benchmark interest rate and is the rate at which the RBI lends money to the banks for a short term. Here, the central bank purchases security.

Key Points

- Internal Benchmark Lending Rate (IBLR):

- The Internal Benchmark Lending Rates are a set of reference lending rates which are calculated after considering factors like the bank's current financial overview, deposits and non performing assets (NPAs) etc. BPLR, Base rate, MCLR are the examples of Internal Benchmark Lending Rate.

- Benchmark Prime Lending Rate (BPLR):

- BPLR was used as a benchmark rate by banks for lending till June 2010.

- Under it, bank loans were priced on the actual cost of funds.

- However, the BPLR was subverted, resulting in an opaque system. The bulk of wholesale credit (loans to corporate customers) was contracted at sub-BPL rates and it comprised nearly 70% of all bank credit.

- Under this system, banks were subsidising corporate loans by charging high interest rates from retail and small and medium enterprise customers.

- Base Rate:

- Loans taken between June 2010 and April 2016 from banks were on base rate.

- During the period, base rate was the minimum interest rate at which commercial banks could lend to customers.

- Base rate is calculated on three parameters — the cost of funds, unallocated cost of resources and return on net worth.

- Hence, the rate depended on individual banks and they changed it whenever their cost of funds and other parameters changed.

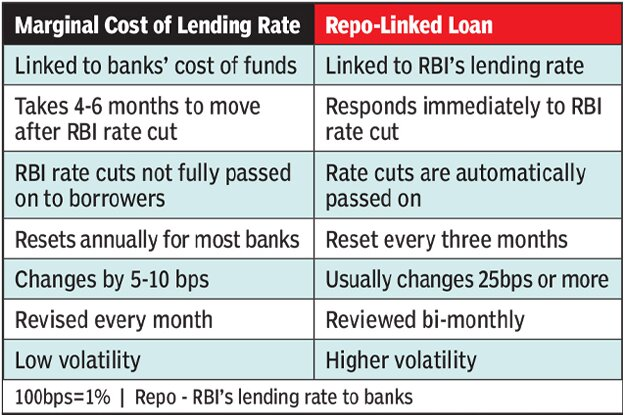

- Marginal Cost of Lending Rate (MCLR):

- It came into effect in April 2016. It is a benchmark lending rate for floating-rate loans. This is the minimum interest rate at which commercial banks can lend.

- This rate is based on four components—the marginal cost of funds, negative carry on account of cash reserve ratio, operating costs and tenor premium.

- MCLR is linked to the actual deposit rates. Hence, when deposit rates rise, it indicates the banks are likely to hike MCLR and lending rates are set to go up.

- Issues Related to IBLR Linked Loans:

- The problem with the IBLR regime was that when RBI cut the repo and reverse repo rates, banks did not pass the full benefits to borrowers.

- In the IBLR Linked Loans, the interest rate has many variables including bank’s spread, their current financial overview, deposits and non performing assets (NPAs) etc.

- Due to this, such internal benchmarks did little to facilitate any swift change in interest rates as per changes in RBI repo rate policy.

- The opacity in interest rate setting processes under internal benchmark regime hinders transmission to lending rates.

- EBLR and Its Benefits:

- About:

- To ensure complete transparency and standardization, RBI mandated the banks to adopt a uniform external benchmark within a loan category, effective 1st October, 2019.

- Unlike MCLR which was internal system for each bank, RBI has offered banks the options to choose from 4 external benchmarking mechanisms:

- The RBI repo rate

- The 91-day T-bill yield

- The 182-day T-bill yield

- Anny other benchmark market interest rate as developed by the Financial Benchmarks India Pvt. Ltd.

- T-Bill or Treasury bills are money market instruments issued by the Government of India as a promissory note with guaranteed repayment at a later date.

- Financial Benchmarks India Pvt. Ltd was recognised by the Reserve bank of India as an independent Benchmark administrator on 2nd July 2015.

- Benefits:

- Banks are free to decide the spread over the external benchmark.

- However, the interest rate must be reset as per the external benchmark at least once every three months.

- Being an external system, this means any policy rate cut decision will reach borrowers faster.

- The adoption of external benchmarking will make the interest rates transparent.

- The borrower will also know the spread or profit margin for each bank over the fixed interest rate making loan comparisons easier and more transparent.

- Banks are free to decide the spread over the external benchmark.

- About:

Way Forward

- Higher interest rates offered by competing saving instruments such as small saving schemes and debt mutual fund schemes have impeded transmission especially during the easing cycle.

- Thus, the government should synchronise the Fiscal policy with the monetary policy in the long-term.