ARCs for Agriculture Sector | 06 Dec 2021

Why in News

To improve recovery of bad loans in the agriculture sector, leading banks have made a pitch for setting up an Asset Reconstruction Company (ARC) specifically to deal with collections and recovery of farm loans.

- With a government-backed ARC having been recently set up to deal with bank NPAs to the industry, this idea has acceptability among banks.

- Some member banks of the Indian Banks' Association suggested the need for the Central government to bring legislation on agriculture land somewhat like the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002.

Key Points

- About the Asset Reconstruction Company (ARC):

- Objective: It is a specialized financial institution that buys the Non Performing Assets (NPAs) from banks and financial institutions so that they can clean up their balance sheets.

- This helps banks to concentrate in normal banking activities. Banks, rather than going after the defaulters by wasting their time and effort, can sell the bad assets to the ARCs at a mutually agreed value.

- Legal Basis: The SARFAESI Act, 2002 provides the legal basis for the setting up of ARCs in India.

- The Act helps reconstruction of bad assets without the intervention of courts. Since then, a large number of ARCs were formed and were registered with the Reserve Bank of India (RBI) which has got the power to regulate the ARCs.

- Funding: To meet its funding requirements, an ARC can issue bonds, debentures and security receipts.

- National Asset Reconstruction Company Limited (NARCL):

- In the Budget 2021-22, ARC has been proposed to be set up by state-owned and private sector banks, and there will be no equity contribution from the government.

- The ARC, which will have an Asset Management Company (AMC) to manage and sell bad assets, will look to resolve stressed assets of Rs. 2-2.5 lakh crore that remain unresolved in around 70 large accounts.

- This is being considered as the government's version of a bad bank.

- Objective: It is a specialized financial institution that buys the Non Performing Assets (NPAs) from banks and financial institutions so that they can clean up their balance sheets.

- Need of ARC for Farm Loans:

- NPAs of Banks: As per the latest Financial Stability Report, June 2021, banks’ gross NPA ratio for the agriculture sector was at 9.8%, whereas for industry and services it was at 11.3% and 7.5%, respectively, At March-end 2021.

- Outstanding Loans: As per data from the ‘Situation Assessment of Agricultural Households and Land Holdings of Households in Rural India, 2019, even as the percentage of agricultural households indebted has come down from 52% in 2013 to 50.2% in 2019, the average debt has jumped by more than 57% from Rs 47,000 in 2013 Rs 74,121 in 2019.

- The survey data shows that 69.6 % of the outstanding loans by agricultural households were taken from institutional sources such as banks, cooperative societies, and other government agencies.

- The survey is conducted by the National Statistical Office’s (NSO).

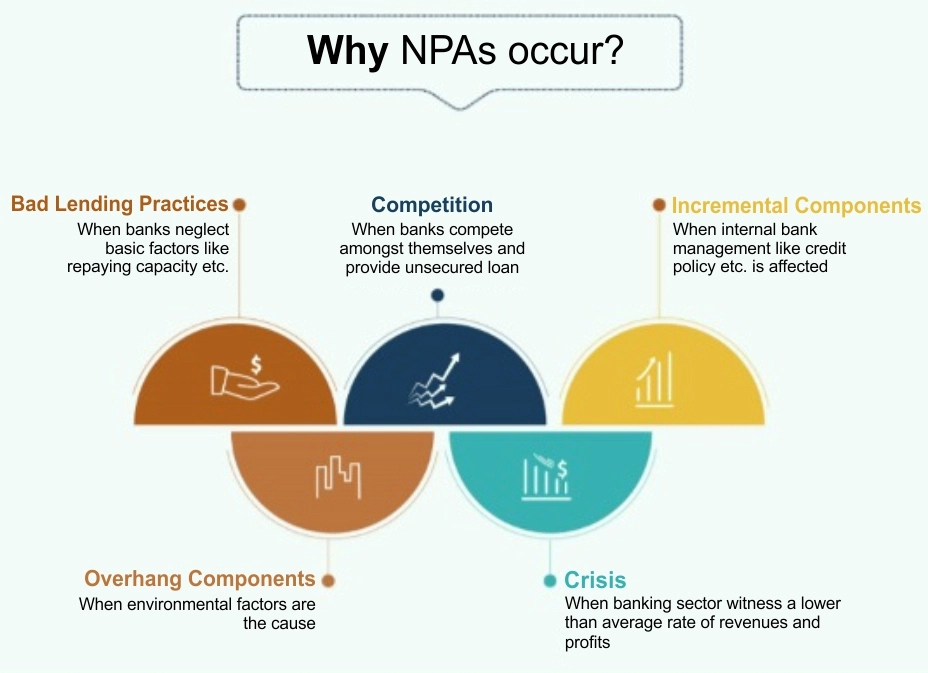

- Farm Loan Waivers: The announcement of farm loan waivers by states around elections leads to “deteriorating credit culture”.

- Since 2014, at least 11 states have announced farm loan waivers. These include Rajasthan, Madhya Pradesh, Punjab, Chhattisgarh, Andhra Pradesh, Telangana, Maharashtra, Punjab and Uttar Pradesh.

- The Uttar Pradesh government will provide additional incentives such as subsided interest rates on farm loans, promotion of farm-based industries as well as development of farm infrastructure under the Centre’s Agriculture Infrastructure Fund.

- The Agriculture Infrastructure Fund aims to provide medium-long term debt financing facilities for investment in viable projects for post-harvest management Infrastructure and community farming assets.

- Ahead of Assembly elections in seven states in 2021, there is a concern among banks that NPAs may rise in the farm sector.

- While genuine hardship could be one reason for delay in repayments, the possibility of waivers also leads to recovery challenges for the banks.

- NPAs of Banks: As per the latest Financial Stability Report, June 2021, banks’ gross NPA ratio for the agriculture sector was at 9.8%, whereas for industry and services it was at 11.3% and 7.5%, respectively, At March-end 2021.

- Challenges:

- Availability of Funds: First and foremost, the requirement of the ARC is to have sufficient availability of funds to match the huge amount of the NPA market.

- It will be welcomed if the government establishes ARC with an equity contribution from the government itself and the Reserve Bank of India (RBI) to strengthen its capital base.

- Thus ARC will have sufficient funds to deal with the NPA problem.

- Absence of a Vibrant Distressed Debt Market: Even if sufficient funds are available with ARC, the price expectation mismatch between selling bank (s) and buying ARC and agreement on an acceptable valuation of the bad assets will also create a challenge for ARC.

- It is the absence of a vibrant distressed debt market in India. It is also difficult to sell NPA assets in the market.

- Absence of Professional Expertise: The absence of professional expertise for a turnaround in ARC is very common.

- The professionals such as bankers, lawyers and chartered accountants who join ARCs usually expect some extra return.

- But due to regulatory issues, this is not possible easily and ARC is deprived of professionals’ service of experts which may help it tremendously.

- Absence of Mature Secondary Market: There is the absence of a mature secondary market for security receipts (SR) issued by ARC to Qualified Institutional Buyers.

- This further leads the Banks to buy SRs backed by their own stressed assets.

- It is observed that currently, over 80% of SRs are held by seller banks themselves only.

- Regulatory Constraints: Currently, all ARCs are subject to the regulation and scrutiny of the regulator i.e. the RBI and it is observed that some stringent regulations have hampered their growth and viability. Thus, the ARC is not being able to function with all its potentials.

- Availability of Funds: First and foremost, the requirement of the ARC is to have sufficient availability of funds to match the huge amount of the NPA market.

Current Mechanism to tackle NPAs of Agri-Sector:

- At present, there is neither a unified mechanism to tackle NPAs in the farm sector nor a single law that deals with enforcement of mortgages created on agricultural land.

- Agriculture being a state subject, the recovery laws, wherever agricultural land is offered as collateral – varies from state to state.

- Enforcement of provisions on mortgaged farm land is generally done through the Revenue Recovery Act of states, Recovery of Debt and Bankruptcy Act, 1993, among other state-specific regulations.

- These are often time consuming and in some states revenue recovery laws covering bank loans have not been enacted.

Way Forward

- It is utmost necessary for a rigorous and a realistic approach to pricing between the banks and ARCs.

- Therefore, it is an urgent need for all stakeholders, including the regulator, to come together to make the entire process of NPA sale, resolution, recovery and revival fast and smooth.

- Banks have their hands tied when it comes to recovery of loans in the agriculture sector. There is also a problem of anticipated farm loans waivers, which makes recovery difficult.

- The ARC has a very vital role to play in the current scenario and it should be strengthened to solve the massive NPA problem prevailing in the Indian banking industry.

- However, ARC cannot be the sole response. The most efficient approach would be to design solutions tailor-made for different parts of India’s bad loan problem and use ARC only as a last resort once all other methods fail.