Governance

15th Finance Commission Recommendations: Resource Allocation

- 03 Feb 2021

- 8 min read

Why in News

Recently, the government accepted the 15th Finance Commission’s recommendation to maintain the States’ share in the divisible pool of taxes to 41% for the five-year period starting 2021-22.

- The Commission’s Report was tabled in the Parliament.

15th Finance Commission

- The Finance Commission (FC) is a constitutional body, that determines the method and formula for distributing the tax proceeds between the Centre and states, and among the states as per the constitutional arrangement and present requirements.

- Under Article 280 of the Constitution, the President of India is required to constitute a Finance Commission at an interval of five years or earlier.

- The 15th Finance Commission was constituted by the President of India in November 2017, under the chairmanship of NK Singh. Its recommendations will cover a period of five years from the year 2021-22 to 2025-26.

Key Points

- Vertical Devolution (Devolution of Taxes of the Union to States):

- It has recommended maintaining the vertical devolution at 41% - the same as in its interim report for 2020-21.

- It is at the same level of 42% of the divisible pool as recommended by the 14th Finance Commission.

- It has made the required adjustment of about 1% due to the changed status of the erstwhile State of Jammu and Kashmir into the new Union Territories of Ladakh and Jammu and Kashmir.

- It has recommended maintaining the vertical devolution at 41% - the same as in its interim report for 2020-21.

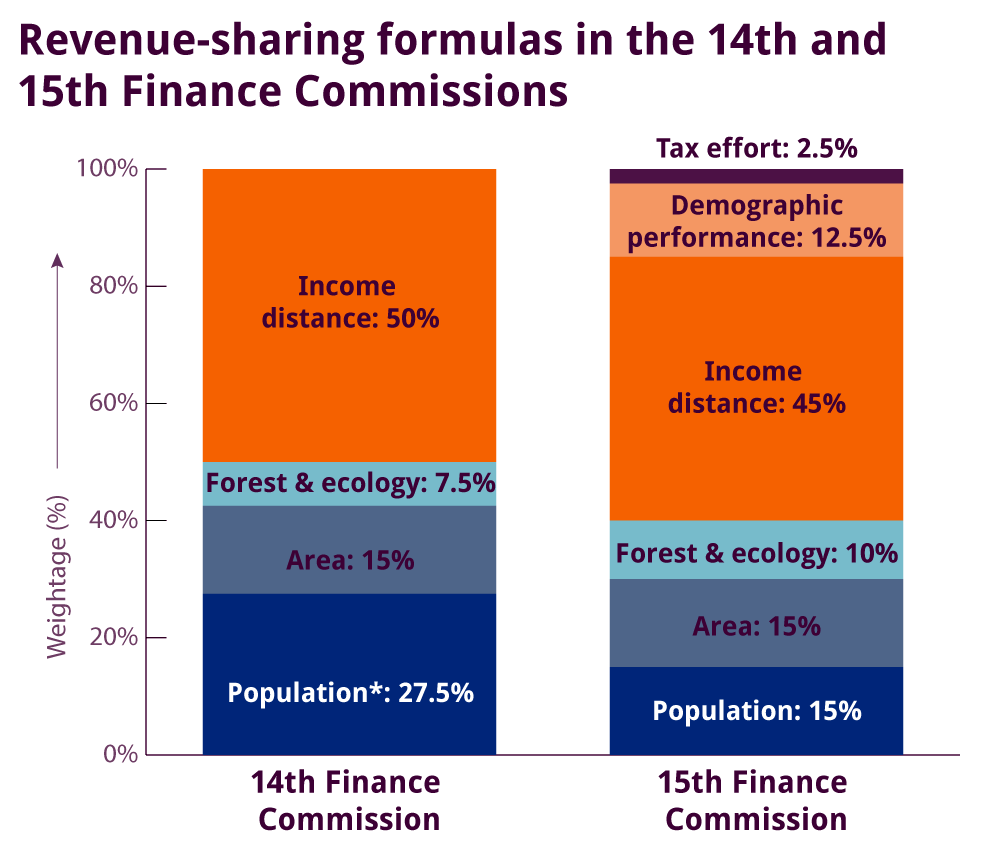

- Horizontal Devolution (Allocation Between the States):

- For horizontal devolution, it has suggested 12.5% weightage to demographic performance, 45% to income, 15% each to population and area, 10% to forest and ecology and 2.5% to tax and fiscal efforts.

- Revenue Deficit Grants to States:

- Revenue deficit grants emanate from the requirement to meet the fiscal needs of the States on their revenue accounts that remain to be met, even after considering their own tax and non-tax resources and tax devolution to them.

- Revenue Deficit is defined as the difference between revenue or current expenditure and revenue receipts, that includes tax and non-tax.

- It has recommended post-devolution revenue deficit grants amounting to about Rs. 3 trillion over the five-year period ending FY26.

- The number of states qualifying for the revenue deficit grants decreases from 17 in FY22, the first year of the award period to 6 in FY26, the last year.

- Performance Based Incentives and Grants to States:

- These grants revolve around four main themes.

- The first is the social sector, where it has focused on health and education.

- Second is the rural economy, where it has focused on agriculture and the maintenance of rural roads.

- The rural economy plays a significant role in the country as it encompasses two-thirds of the country's population, 70% of the total workforce and 46% of national income.

- Third, governance and administrative reforms under which it has recommended grants for judiciary, statistics and aspirational districts and blocks.

- Fourth, it has developed a performance-based incentive system for the power sector, which is not linked to grants but provides an important, additional borrowing window for States.

- Fiscal Space for Centre:

- Total 15th Finance Commission transfers (devolution + grants) constitutes about 34% of estimated Gross Revenue Receipts to the Union, leaving adequate fiscal space to meet its resource requirements and spending obligations on national development priorities.

- Grants to Local Governments:

- Along with grants for municipal services and local government bodies, it includes performance-based grants for incubation of new cities and health grants to local governments.

- In grants for Urban local bodies, basic grants are proposed only for cities/towns having a population of less than a million. For Million-Plus cities, 100% of the grants are performance-linked through the Million-Plus Cities Challenge Fund (MCF).

- MCF amount is linked to the performance of these cities in improving their air quality and meeting the service level benchmarks for urban drinking water supply, sanitation and solid waste management.

Criticism

- Performance based incentives disincentivizes independent decision-making. Any conditions on the state's ability to borrow will have an adverse effect on the spending by the state, particularly on development thus, undermines cooperative fiscal federalism.

- It does not hold the Union government accountable for its own fiscal prudence and dilutes the joint responsibility that the Union and States have.

Horizontal Devolution Criteria

- Population:

- The population of a State represents the needs of the State to undertake expenditure for providing services to its residents.

- It is also a simple and transparent indicator that has a significant equalising impact.

- Area:

- The larger the area, greater is the expenditure requirement for providing comparable services.

- Forest and Ecology:

- By taking into account the share of dense forest of each state in the aggregate dense forest of all the states, the share on this criteria is determined.

- Income Distance:

- Income distance is the distance of the Gross State Domestic Product (GSDP) of a particular state from the state with the highest GSDP.

- To maintain inter state equity, the states with lower per capita income would be given a higher share.

- Demographic Performance:

- It rewards efforts made by states in controlling their population.

- This criterion has been computed by using the reciprocal of the total fertility ratio of each state, scaled by 1971 population data.

- This has been done to assuage the fears of southern States about losing some share in tax transfers due to the reliance on the 2011 Census data instead of the 1971 census, which could penalise States that did better on managing demographics.

- States with a lower fertility ratio will be scored higher on this criterion.

- The Total Fertility Ratio in a specific year is defined as the total number of children that would be born to each woman if she/they were to pass through the childbearing years bearing children according to a current schedule of age-specific fertility rates.

- Tax Effort:

- This criterion has been used to reward states with higher tax collection efficiency.

- It has been computed as the ratio of the average per capita own tax revenue and the average per capita state GDP during the three-year period between 2016-17 and 2018-19.