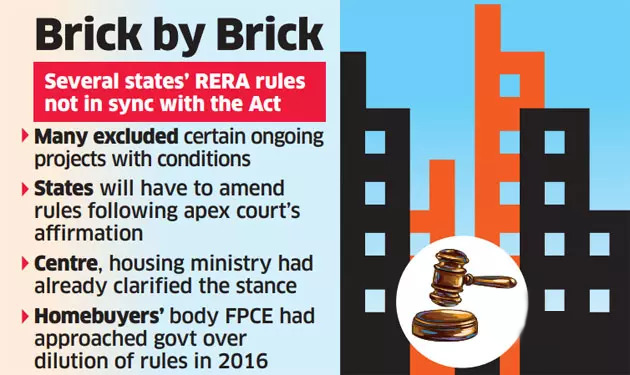

RERA is Retroactive: SC

Why in News

Recently, the Supreme Court (SC) interpreted that the Real Estate (Regulation and Development) Act, 2016 (RERA) is retroactive.

- The SC’s ruling is aimed at protecting homebuyers, the ruling brings a major relief for the buyers, speeds up the resolution process, and makes it difficult for state governments to dilute the intent of the law.

Key Points

- Retroactive Implementation:

- The SC affirmed that the provisions of the RERA 2016 are applicable to projects that were ongoing and for whom completion certificates were not obtained at the time of the enactment of the law.

- Under the Act, registration of real estate projects was mandatory.

- It mandated that for projects that were ongoing on the date of commencement of the Act, specifically projects for which the completion certificate had not been issued, the promoters shall be under obligation to make an application to the authority for registration of the project.

- Regulations of RERA authorities in states including Uttar Pradesh, Haryana, Punjab, Karnataka, Telangana and Tamil Nadu are currently not in line with this position and may need to amend their rules to ensure all ongoing projects get covered under RERA.

- The SC affirmed that the provisions of the RERA 2016 are applicable to projects that were ongoing and for whom completion certificates were not obtained at the time of the enactment of the law.

- Recovery of Invested Amount:

- SC also held that the amount invested by the allottees, along with interest as quantified by the regulatory authority or the adjudicating officer, can be recovered as arrears of land revenue from the builders.

- The builders had contended that homebuyers are only entitled to recover interest or penalty as arrears of land.

- However, taking into consideration the scheme of the Act, the court observed, what is to be returned to the allottee is his own life savings. The amount with interest as computed/quantified by the authority becomes recoverable and such arrear becomes enforceable in law.

- SC also held that the amount invested by the allottees, along with interest as quantified by the regulatory authority or the adjudicating officer, can be recovered as arrears of land revenue from the builders.

- Penalty for Developers:

- It is mandatory for real estate developers to deposit at least 30% of the penalty ordered by the regulator, or the full amount as the case may be, before they challenge any RERA order. This is expected to ensure that only genuine appeals are filed and homebuyers’ interests are protected.

- SC noted that the obligation cast upon the promoter of pre-deposit under the Act, in no circumstance can be said to be in violation of Article 14 (Equality before law) or Article 19 1(g)(freedom to practise any profession, or to carry on any occupation, trade or business) of the Constitution of India.

- Builders/promoters who are in appeal are required to make the predeposit to get the appeal entertained by the Appellate Tribunal.

- A promoter is defined as a person who is entrusted with the task of promoting the project (real estate project), which was developed or constructed by the developer.

- The intention of the legislature appears to be to ensure that the rights of the decree holder (the successful party) is to be protected and only genuine bonafide appeals are to be entertained.

- SC noted that the obligation cast upon the promoter of pre-deposit under the Act, in no circumstance can be said to be in violation of Article 14 (Equality before law) or Article 19 1(g)(freedom to practise any profession, or to carry on any occupation, trade or business) of the Constitution of India.

- It is mandatory for real estate developers to deposit at least 30% of the penalty ordered by the regulator, or the full amount as the case may be, before they challenge any RERA order. This is expected to ensure that only genuine appeals are filed and homebuyers’ interests are protected.

Real Estate Regulation and Development Act, 2016

- Need:

- Securing the Largest Investment Sector: Regulation of the real estate sector was under discussion since 2013, and the RERA Act eventually came into being in 2016. Data show that more than 77% of the total assets of an average Indian household are held in real estate, and it’s the single largest investment of an individual in his lifetime.

- Creating Accountability: Prior to the law, the real estate and housing sector was largely unregulated, with the consequence that consumers were unable to hold builders and developers accountable.

- The Consumer Protection Act, 1986 was inadequate to address the needs of homebuyers.

- RERA was introduced with the objective of ensuring greater accountability towards consumers, to reduce frauds and delays, and to set up a fast track dispute resolution mechanism.

- Major Provisions:

- Establishment of state level regulatory authorities- Real Estate Regulatory Authority (RERA): The Act provides for State governments to establish more than one regulatory authority with the following mandate:

- Register and maintain a database of real estate projects; publish it on its website for public viewing,

- Protection of interest of promoters, buyers and real estate agents

- Development of sustainable and affordable housing,

- Render advice to the government and ensure compliance with its Regulations and the Act.

- Establishment of Real Estate Appellate Tribunal- Decisions of RERAs can be appealed in these tribunals.

- Mandatory Registration: All projects with plot size of minimum 500 sq.mt or eight apartments need to be registered with Regulatory Authorities.

- Deposits: Depositing 70% of the funds collected from buyers in a separate escrow bank account for construction of that project only.

- Liability: Developer’s liability to repair structural defects for five years.

- Penal interest in case of default: Both promoter and buyer are liable to pay an equal rate of interest in case of any default from either side.

- Cap on Advance Payments: A promoter cannot accept more than 10% of the cost of the plot, apartment or building as an advance payment or an application fee from a person without first entering into an agreement for sale.

- Carpet Area: Defines Carpet Area as net usable floor area of flat. Buyers will be charged for the carpet area and not the super built-up area.

- Punishment: Imprisonment of up to three years for developers and up to one year in case of agents and buyers for violation of orders of Appellate Tribunals and Regulatory Authorities.

- Establishment of state level regulatory authorities- Real Estate Regulatory Authority (RERA): The Act provides for State governments to establish more than one regulatory authority with the following mandate:

- Implementation of the Act:

- 34 states/Union Territories have notified rules under RERA, while its implementation in Nagaland is under process.

- West Bengal has enacted its own legislation — West Bengal Housing Industry Regulation Act, 2017 (HIRA) — instead of notifying rules under RERA.

- 30 States/UTs have set up Real Estate Regulatory Authorities, and 26 have set up Real Estate Appellate Tribunals, as per the latest data available with the Ministry of Housing and Urban Affairs.

Proposed Norms for Digital Lending: RBI

Why in News

Recently, the Reserve Bank of India (RBI) Working Group (WG) Committee has made recommendations pertaining to Digital Lending, including a separate legislation to prevent illegal digital lending activities.

- The RBI constituted a WG on digital lending including lending through online platforms and mobile apps in January, 2021.

- The panel was set up in the backdrop of business conduct and customer protection concerns arising out of the spurt in digital lending activities.

Key Points

- About:

- The RBI says lending through digital mode relative to physical mode is still at a nascent stage in the case of banks (Rs 1.12 lakh crore via digital mode against Rs 53.08 lakh crore through the physical mode).

- Whereas for Non-Banking Financial Companies (NBFCs), a higher proportion of lending (Rs 0.23 lakh crore via digital mode against Rs 1.93 lakh crore through the physical mode) is happening through digital mode.

- While banks have been increasingly adopting innovative approaches in digital processes, NBFCs have been at the forefront of partnered digital lending.

- Key Proposals:

- Digital lending apps should be subjected to a verification process by a nodal agency to be set up in consultation with stakeholders.

- To set up a Self-Regulatory Organisation (SRO) covering the participants in the digital lending ecosystem.

- The use of unsolicited commercial communications for digital loans to be governed by a code of conduct to be put in place by the proposed SRO.

- The maintenance of a ‘negative list’ of lending service providers by the proposed SRO.

- Disbursement of loans should be directly into bank accounts of borrowers.

- All data to be stored in servers located in India.

- Algorithmic features used in digital lending to be documented should ensure necessary transparency.

Digital Lending

- About:

- It consists of lending through web platforms or mobile apps, by taking advantage of technology for authentication and credit assessment.

- Banks have launched their own independent digital lending platforms to tap in the digital lending market by leveraging existing capabilities in traditional lending.

- Significance:

- Financial Inclusion: It helps in meeting the huge unmet credit need, particularly in the microenterprise and low-income consumer segment in India.

- Reduce Borrowing from informal channels: It helps in reducing informal borrowings as it simplifies the process of borrowing.

- Time Saving: It decreases time spent on working loan applications in-branch. Digital lending platforms have also been known to cut overhead costs by 30-50%.

- Challenges:

- Growing number of unauthorised digital lending platforms and mobile applications as:

- They charge excessive rates of interest and additional hidden charges.

- They adopt unacceptable and high-handed recovery methods.

- They misuse agreements to access data on mobile phones of borrowers.

- Growing number of unauthorised digital lending platforms and mobile applications as:

- Steps Taken by RBI:

- Non-Banking Financial Companies (NBFCs) and banks need to state the names of online platforms they are working with.

- RBI has also mandated that digital lending platforms which are used on behalf of Banks and NBFCs should disclose the name of the Bank(s) or NBFC(s) upfront to the customers.

- The central bank had also asked lending apps to issue a sanction letter to the borrower on the letter head of the bank/ NBFC concerned before the execution of the loan agreement.

- Legitimate public lending activities can be undertaken by banks, NBFCs registered with the RBI and other entities who are regulated by state governments under statutory provisions.

- Ease Reforms.

- India's Digital Ecosystem:

- Nearly 72% of financial transactions of Public Sector Banks (PSBs) are done through digital channels, with doubling of customers active on digital channels from 3.4 crore in FY 2019-20 to 7.6 crore in FY 2020-21.

- The share of financial transactions undertaken through home and mobile channels has increased from 29% in FY 2018-19 to 76% in FY 2020-21.

Way Forward

- India is on the verge of a digital lending revolution and making sure that this lending is done responsibly can ensure the fruits of this revolution are realized.

- As several players have access to sensitive consumer data, there must be clear guidelines around, for example, the type of data that can be held, the length of time data can be held for, and restrictions on the use of data.

- Digital lenders should proactively develop and commit to a code of conduct that outlines the principles of integrity, transparency and consumer protection, with clear standards of disclosure and grievance redressal.

- An agency can be created that tracks all digital loans and consumer/lender credit history.

- Apart from establishing technological safeguards, educating and training customers to spread awareness about digital lending is also important.

Continuation of PMGSY I and II and RCPLWEA

Why in News

The Cabinet Committee on Economic Affairs (CCEA) gave its approval for continuation of Pradhan Mantri Gram Sadak Yojana-I and II (PMGSY-I and II) upto September, 2022 for completion of balance road and bridge works.

- The CCEA also approved continuation of Road Connectivity Project for Left Wing Extremism Affected Areas (RCPLWEA) upto March, 2023.

Key Points

- PMGSY:

- PMGSY-I:

- Centrally Sponsored Scheme, launched in the year 2000 to provide connectivity to eligible unconnected habitations of 500+ in plain areas and 250+ in North-East and Himalayan states as per census 2001.

- The Scheme also included a component of upgradation of existing rural roads for those districts where all the eligible habitations had been saturated.

- PMGSY-II:

- It was approved by the Cabinet in May, 2013, envisaged consolidation of 50,000 Km of existing rural road network.

- PMGSY-III:

- It was launched in the year 2019 for consolidation of 1,25,000 Km existing through routes and major rural links connecting habitations, inter-alia, to Gramin Agricultural Markets, Higher Secondary Schools and Hospitals.

- The implementation period of the scheme is upto March, 2025.

- PMGSY-I:

- Road Connectivity Project for Left Wing Extremism Affected Areas:

- It was launched in 2016 for construction/upgradation of 5,412 Km road length and 126 bridges of strategic importance in 44 districts in 9 states, viz. Andhra Pradesh, Bihar, Chhattisgarh, Jharkhand, Madhya Pradesh, Maharashtra, Odisha, Telangana and Uttar Pradesh.

- Implementation period was 2016-17 to 2019-20.

- Road and bridge works to be taken up under the scheme have been identified by the Ministry of Home Affairs in consultation with states and security forces.

- Significance:

- Various independent impact evaluation studies carried out on PMGSY have concluded that the scheme has had a positive impact on agriculture, health, education, urbanization and employment generation, etc.

- Rural Connectivity is a development imperative.

- All weather road connectivity to balance habitations would unlock the economic potential of the connected habitations.

- Upgradation of the existing rural roads would improve the overall efficiency of the road network as a provider of transportation services for people, goods and services.

- The construction/upgradation of roads would generate both direct and indirect employment to the local populace.

- Challenges:

- Lack of dedicated funds.

- Limited involvement of the Panchayati Raj Institutions.

- Inadequate execution and contracting capacity.

- Less working season and difficult terrain particularly in Hill States.

- Scarcity of the construction materials.

- Security concerns particularly in Left Wing Extremism (LWE) areas.

Way Forward

Rural Road Connectivity is a key component of Rural Development as it promotes access to economic and social services. Further, it helps in generating increased agricultural incomes and productive employment opportunities in India. In this regard, the government can consider engagement with international financial institutions to construct basic rural infrastructure.

India Becomes the Highest Recipient of Remittances

Why in News

According to the World Bank’s Migration and Development Brief, India has become the world’s largest recipient of Remittances, receiving USD 87 billion (a gain of 4.6 % from previous year) in 2021.

- India is followed by China, Mexico, the Philippines, and Egypt.

- The United States being the biggest source, accounting for over 20% of all Remittances.

Key Points

- Factors for Remittance Growth:

- Migrants’ determination to support their families in times of need, aided by economic recovery in Europe and the United States which in turn was supported by the Fiscal Stimulus and employment support programs.

- In the Gulf Cooperation Council (GCC) countries and Russia, the recovery of outward remittances was also facilitated by stronger oil prices and the resulting pickup in economic activity.

- The severity of Covid-19 caseloads and deaths during the second quarter (well above the global average) played a prominent role in drawing substantial flows (including for the purchase of oxygen tanks) to the country.

- Flows from migrants have greatly complemented government cash transfer programs to support families suffering economic hardships during the Covid-19 crisis.

- Projection for 2022:

- Remittances are projected to grow 3% in 2022 to USD 89.6 billion, because of a drop in overall migrant stock, as a large proportion of returnees from the Arab countries await return.

- Other Countries:

- Remittances registered strong growth in most regions.

- Latin America and Caribbean (21.6 %), Middle East and North Africa (9.7 %), South Asia (8 %), Sub-Saharan Africa (6.2 %), Europe and Central Asia (5.3 %).

- In East Asia and the Pacific, remittances fell by 4 % - though excluding China, remittances registered a gain of 1.4 % in the region.

- Factors: In Latin America and the Caribbean, growth was exceptionally strong due to economic recovery in the United States and additional factors, including migrants’ responses to natural disasters in their countries of origin and remittances sent from home countries to migrants in transit.

- Remittances registered strong growth in most regions.

- Suggestions:

- To keep remittances flowing, especially through digital channels, providing access to bank accounts for migrants and remittance service providers remains a key requirement.

- Policy responses also must continue to be inclusive of migrants especially in the areas of access to vaccines and protection from underpayment.

World Bank’s Migration and Development Brief

- This is prepared by the Migration and Remittances Unit, Development Economics (DEC)- the premier research and data arm of the World Bank. .

- The brief aims to provide an update on key developments in the area of migration and remittance flows and related policies over the past six months.

- It also provides medium-term projections of remittance flows to developing countries..

- The brief is produced twice a year.

Remittances

- Remittances are usually understood as financial or in-kind transfers made by migrants to friends and relatives back in communities of origin.

- These are basically sum of two main components - Personal Transfers in cash or in kind between resident and non-resident households and Compensation of Employees, which refers to the income of workers who work in another country for a limited period of time.

- Remittances help in stimulating economic development in recipient countries, but this can also make such countries over-reliant on them.

The Sydney Dialogue

Why in News

Recently, the Prime Minister delivered the keynote at the inaugural Sydney Dialogue via video conferencing.

- He spoke on the theme of India’s technology evolution and revolution.

Key Points

- Highlights of the Address:

- The international order should ensure cryptocurrencies do not end up in the wrong hands.

- Citing the unregulated nature of the crypto market, recently, the PM called for taking progressive and forward-looking steps.

- India’s space sector is open to private investment and the agriculture sector is reaping the benefits of the digital revolution.

- In 2020, the government opened Indian National Space Promotion and Authorization Centre (IN-SPACe) to provide a level playing field for private companies to use Indian space infrastructure.

- Highlighted the leaps in India’s digital revolution that has redefined politics, economy and society.

- However, the digital age is raising new questions on sovereignty, governance, ethics, law, rights and security.

- The international order should ensure cryptocurrencies do not end up in the wrong hands.

- Five Important Transitions listed by India:

- One, the world's most extensive public information infrastructure being built in India.

- Over 1.3 billion Indians have a unique digital identity (Aadhaar), six hundred thousand villages will soon be connected with broadband and the world's most efficient payment infrastructure, the Unified Payments Interface (UPI).

- Two, use of digital technology for governance, inclusion, empowerment, connectivity, delivery of benefits and welfare.

- Examples: Pradhan Mantri Jan-Dhan Yojana (PMJDY), Common Services Centres (CSC) etc.

- Three, India has the world's third largest and fastest growing Startup Ecosystem.

- Four, India's industry and services sectors, even agriculture, are undergoing massive digital transformation.

- Example: Government e-Marketplace (GeM), agri-startups, etc.

- Five, there is a large effort to prepare India for the future.

- Investing in developing indigenous capabilities in telecom technology such as 5G and 6G.

- India is one of the leading nations in artificial intelligence and machine learning, especially in human-centred and ethical use of artificial intelligence.

- Developing strong capabilities in Cloud platforms and cloud computing.

- One, the world's most extensive public information infrastructure being built in India.

Sydney Dialogue

- It is an initiative of the Australian Strategic Policy Institute.

- It is an annual summit of cyber and critical technologies to discuss the fallout of the digital domain on the law and order situation in the world.

Other Such Initiatives

- Eastern Economic Forum:

- EEF was established by the decree of the President of the Russian Federation in the year 2015.

- It serves as a platform for the discussion of key issues in the world economy, regional integration, and the development of new industrial and technological sectors, as well as of the global challenges facing Russia and other nations.

- Future Investment Initiative:

- The Future Investment Initiative (FII) is widely described as “Davos in the desert”. It is Saudi Arabia’s flagship investment conference.

- The informal name derives from the World Economic Forum’s annual meeting that is held in Davos, Switzerland, where world leaders discuss agendas for pressing international issues.

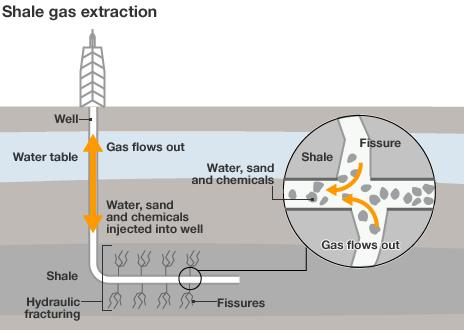

Tight/Shale Oil

Why in News

Cairn India will partner US-based Halliburton to start shale exploration in the Lower Barmer Hill formation, Western Rajasthan.

Key Points

- Shale Oil and Gas:

- Tight Oil: The key difference between shale oil and conventional crude is that the former, also called ‘tight oil’, is found in smaller batches, and deeper than conventional crude deposits.

- Shale Gas: Unlike conventional hydrocarbons that can be extracted from the permeable rocks easily, shale gas is trapped under low permeable rocks.

- Extraction Process: Extraction requires creation of fractures in oil and gas rich shale to release hydrocarbons through a process called hydraulic fracking/fracturing.

- It requires a mixture of ‘pressurised water, chemicals, and sand’ (shale fluid) to break low permeable rocks and have access to the shale gas reserves.

- Top Producers: Russia and the US are among the largest shale oil producers in the world, with a surge in shale oil production in the US having played a key role in turning the country from an importer of crude to a net exporter in 2019.

- Associated Concerns: Shale oil and gas exploration faces several challenges other than environmental concerns around massive water requirements for fracking and potential for groundwater contamination.

- Shale rocks are usually found adjacent to rocks containing usable/ drinking water known as ‘aquifers’.

- While fracking, the shale fluid could possibly penetrate aquifers leading to methane poisoning of groundwater used for drinking and irrigation purposes.

Conventional and Unconventional Resources

- Conventional oil or gas comes from formations that are straightforward to extract product from.

- Extracting fossil fuels from these geological formations can be done with standard methods that can be used to economically remove the fuel from the deposit.

- Conventional resources tend to be easier and less expensive to produce simply because they require no specialized technologies and can utilize common methods.

- Unconventional oil or gas resources are much more difficult to extract.

- Some of these resources are trapped in reservoirs with poor permeability and porosity, meaning that it is extremely difficult or impossible for oil or natural gas to flow through the pores and into a standard well.

- To be able to produce from these difficult reservoirs, specialized techniques and tools are used.

- Prospects of Shale Oil Exploration in India:

- Currently, there is no large-scale commercial production of shale oil and gas in India.

- State-owned ONGC had, in 2013, found prospects of shale oil at the Cambay basin in Gujarat and the Krishna Godavari basin in Andhra Pradesh.

- However, it concluded that the quantity of oil flow observed in these basins did not indicate “commerciality” and that the general characteristics of Indian shales are quite different from North American ones.